On any busy market day in Lagos or Kano, the sound of cash changing hands is increasingly replaced by the soft “ping” of a successful transfer. From market stalls to motor parks, traders now confirm digital payments on their phones instead of counting naira notes. What seemed unlikely a decade ago has become routine.

For millions of informal workers, digital wallets like OPay, PalmPay, and Moniepoint are no longer optional tools. They are central to daily business operations. In 2024, Nigeria recorded over ₦1.07 quadrillion in electronic payment transactions. This shows how deeply digital payments have penetrated the economy.

As mobile money and digital payments continue to expand, Nigeria’s fintech ecosystem is reshaping how value is stored, transferred, and recorded across Africa’s largest economy.

The Mobile Money Surge

Nigeria has become one of Africa’s fastest-growing digital payment markets

The momentum from 2024 continued into 2025, with electronic payments surging to ₦295 trillion in the first quarter alone, representing a 22 percent increase compared to the previous year.

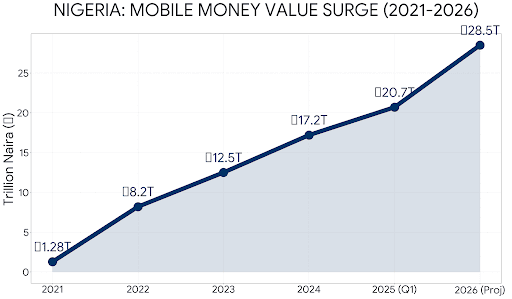

Mobile money transaction value specifically tells an even sharper story. It movedfrom ₦1.28 trillion in 2021 to over ₦20.71 trillion in Q1 2025, reflecting growth of more than 1,500 percent in just four years. At the same time, Point-of-Sale(POS) transactions climbed to ₦10.45 trillion in the first quarter of 2025, recording a 209 percent increase compared to 2024.

These aren’t just figures. They represent people choosing digital money over cash for everyday purchases, from a sachet of pure water to transport fares.

User metrics

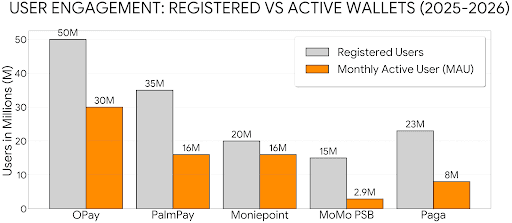

Mobile wallets are no longer apps people download once and ignore. s. Digital wallet providers such as OPay, PalmPay, and Moniepoint are now daily tools for survival and business operations. PalmPay alone now processes approximately 15 million daily transactions with a 99.5 percent success rate, demonstrating both scale and reliability.

MTN Nigeria’s MoMo Payment Service Bank has also shifted towards getting customers who regularly use the wallet for payments and international remittances rather than simply driving registration numbers. By late 2025, MoMo PSB had grown its active wallet base to 2.9 million users. .

With smartphone penetration rising above 66% in 2025, digital finance has been made easy.

Why This Matters for the Informal Economy

The use of cash as a major means of exchange has reduced so far. Cash transactions in Nigeria fell by 59% between 2014 and 2024, showing a preference for digital wallets. a long-term behavioural shift. The 5.9 million active PoS terminals as of March 2025 show how much informal traders now rely on digital channels.

Digital wallets now integrate savings features and embedded credit.. A market trader can access microloans based on digital turnover, an opportunity that traditional banks rarely extended in the past. Digital wallets are also bringing financial inclusion to rural communities. In rural communities where bank branches remain scarce, mobile wallets allow small-scale entrepreneurs and women-led businesses to operate more independently. As one mid-income trader in Damaturu explained, “Before, if you wanted to send money, you had to take a bus to town. Now it’s just on my phone.”

The Policy Engine: Making It All Possible

The Central Bank of Nigeria has contributed to this shift through its Payments System Vision 2025 framework. The launch of the National Payment Stack in November 2025 strengthened instant transfers and interoperability between fintech platforms and banks. At the same time, updated regulatory frameworks have improved consumer protection and fraud detection, increasingly supported by advanced technologies such as artificial intelligence.

New standards for Near Field Communication and QR-based payments have further accelerated contactless transactions in urban centres. These measures have reduced dependence on physical cards and cash while strengthening trust in Nigeria’s digital payment infrastructure.

Where Wallets Are Headed Next

In 2026, digital wallets are evolving beyond simple transfers. The next phase is combining payments, savings, credit, insurance, and cross-border remittances into unified financial ecosystems.

Sub-Saharan Africa continues to lead global mobile money adoption, and Nigeria’s transaction volumes position it as a major driver of that growth.

The trajectory suggests a move toward a predominantly cashless economy where economic identity is increasingly tied to digital transaction history, connecting Nigeria’s informal economy with regional and global financial systems.

Conclusion

Digital wallets are no longer an urban convenience. They are financial lifelines, tools for inclusion, and bridges to credit. For Nigeria’s informal economy, they are not simply transforming transactions, they are reshaping how millions of people participate in and are recognised within the broader financial system.

Enjoying our contents, follow us on our media platforms to get even more interesting contents.

Don’t miss out on what’s trending in tech

Follow Nxt Box